GHG Protocol Corporate Standard and Scope 3 Guidance

Corporate Standard Overview

The GHG Protocol Corporate Standard provides requirements and guidance for companies preparing a corporate-level GHG emissions inventory. It covers accounting and reporting principles, setting organizational boundaries, and establishing operational boundaries.

Key Principles

- Relevance: Ensure the inventory appropriately reflects emissions and serves decision-making needs

- Completeness: Account for and report all GHG emission sources and activities within chosen boundaries

- Consistency: Use consistent methodologies to allow meaningful comparisons over time

- Transparency: Address all relevant issues factually and coherently

- Accuracy: Ensure calculations are systematically neither over nor under actual emissions

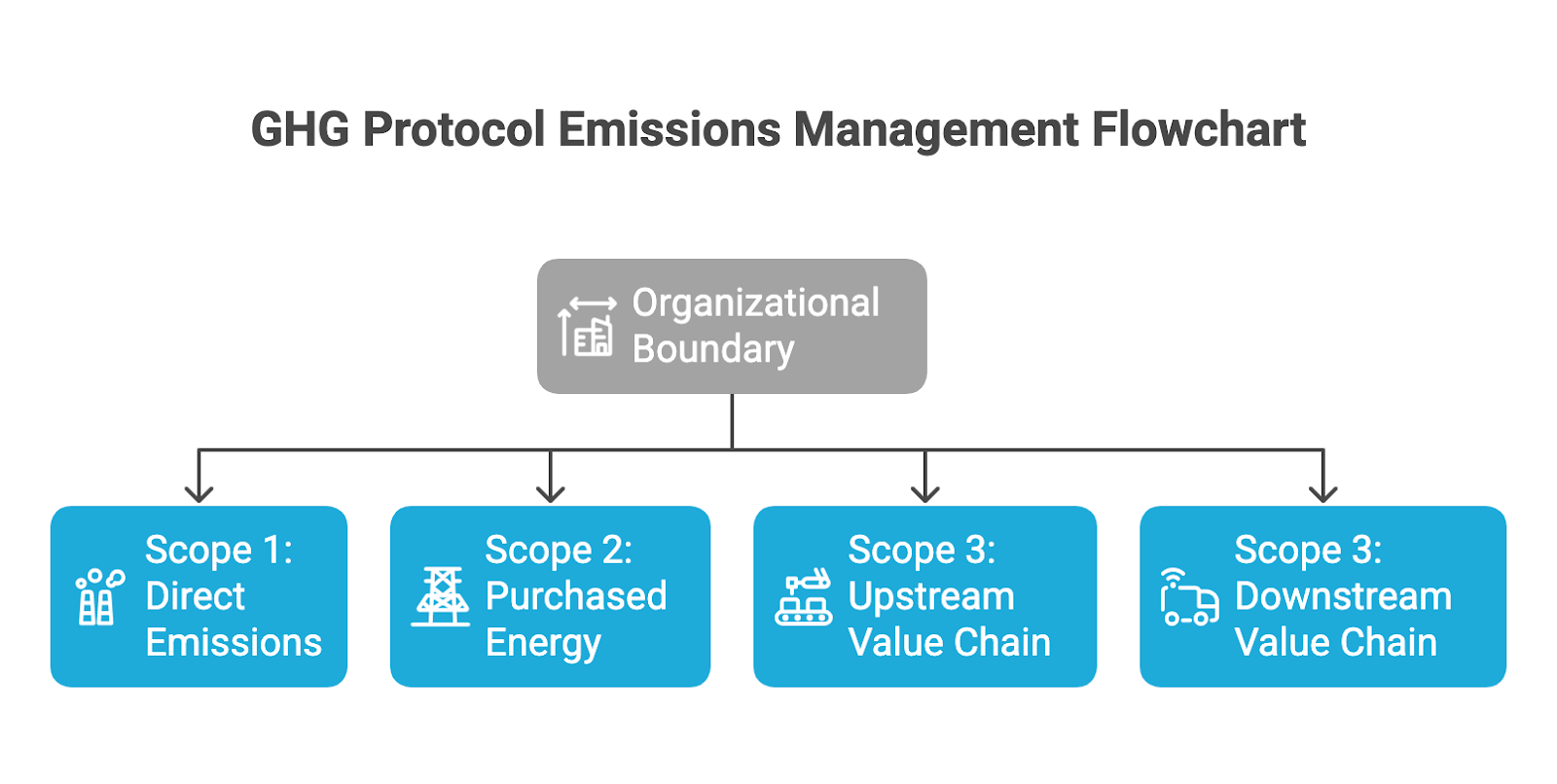

Organizational Boundaries

Companies must choose an approach for consolidating GHG emissions:

- Equity Share: Account for GHG emissions based on share of equity in operations

- Financial Control: Account for GHG emissions from operations over which the company has financial control

- Operational Control: Account for GHG emissions from operations over which the company has operational control

Example: Organizational Boundary Setting

A company owns:

- Manufacturing facility (100% ownership)

- Joint venture facility (40% ownership)

- Leased warehouse (operational control)

Under different approaches:

- Equity Share: 100% of facility 1 emissions + 40% of facility 2 emissions

- Operational Control: 100% of facility 1 and warehouse emissions

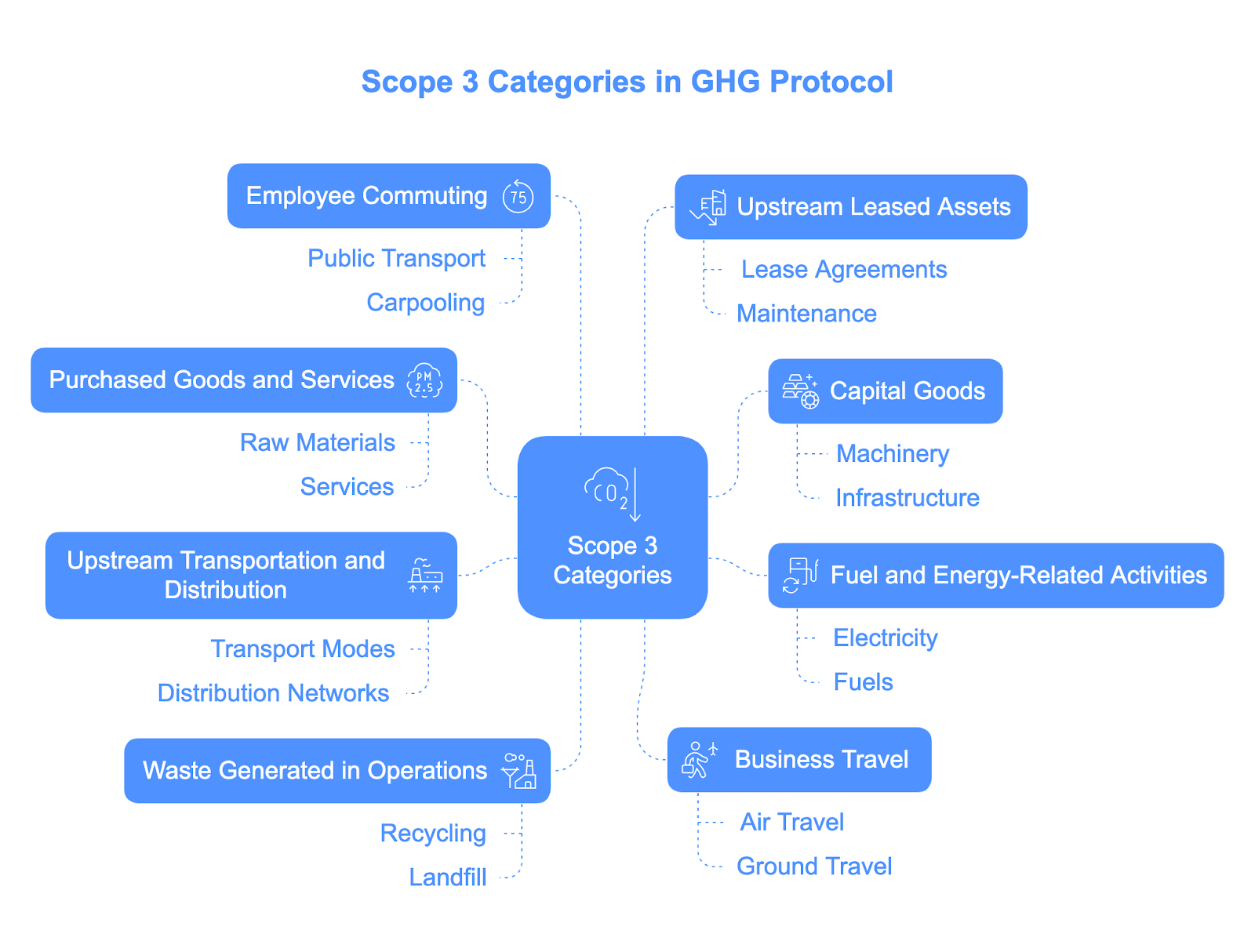

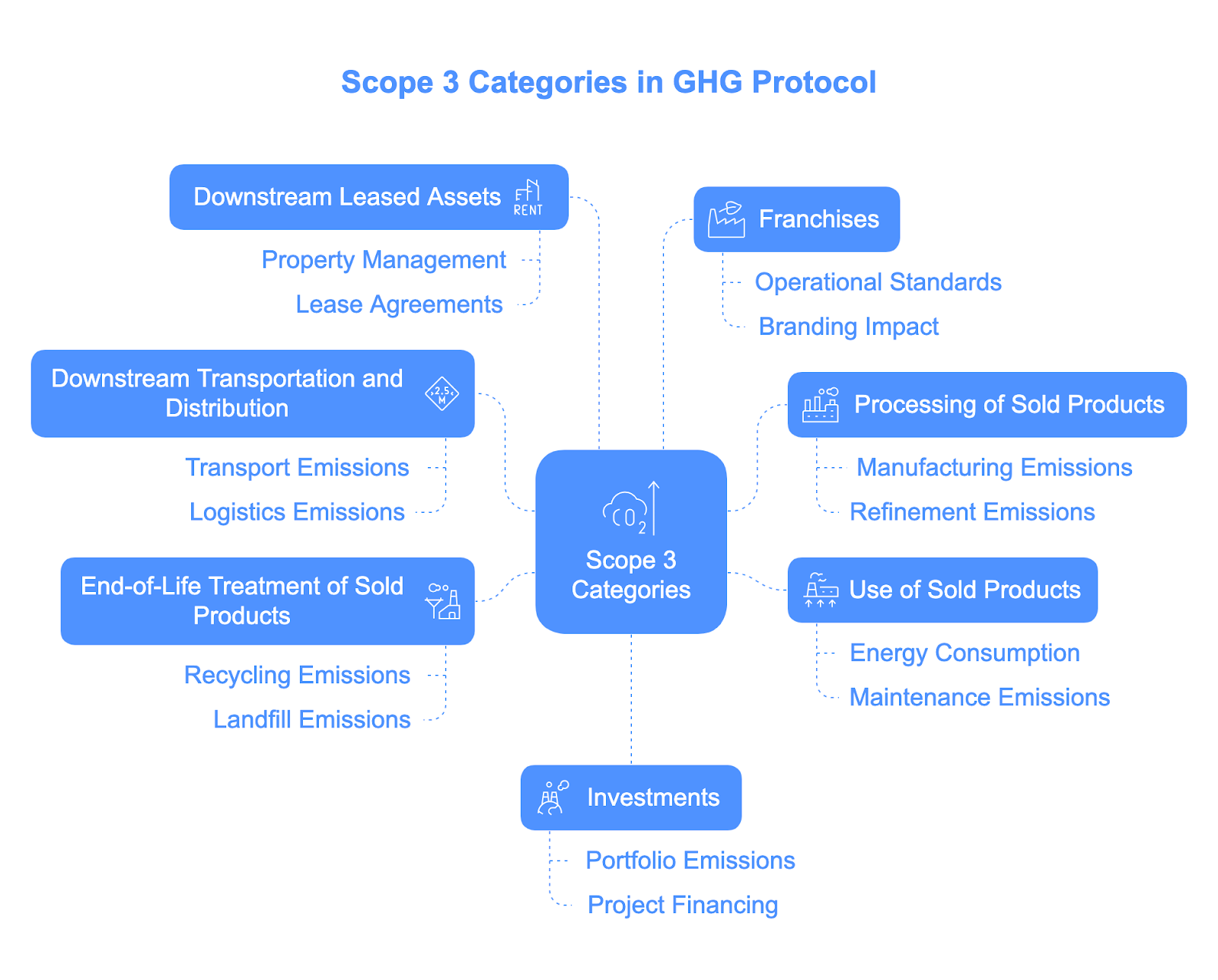

Scope 3 Guidance

The Scope 3 Standard provides requirements and guidance for accounting and reporting value chain emissions. It complements and builds upon the Corporate Standard.

Scope 3 Categories

| Upstream Categories | Downstream Categories |

|

|

Upstream

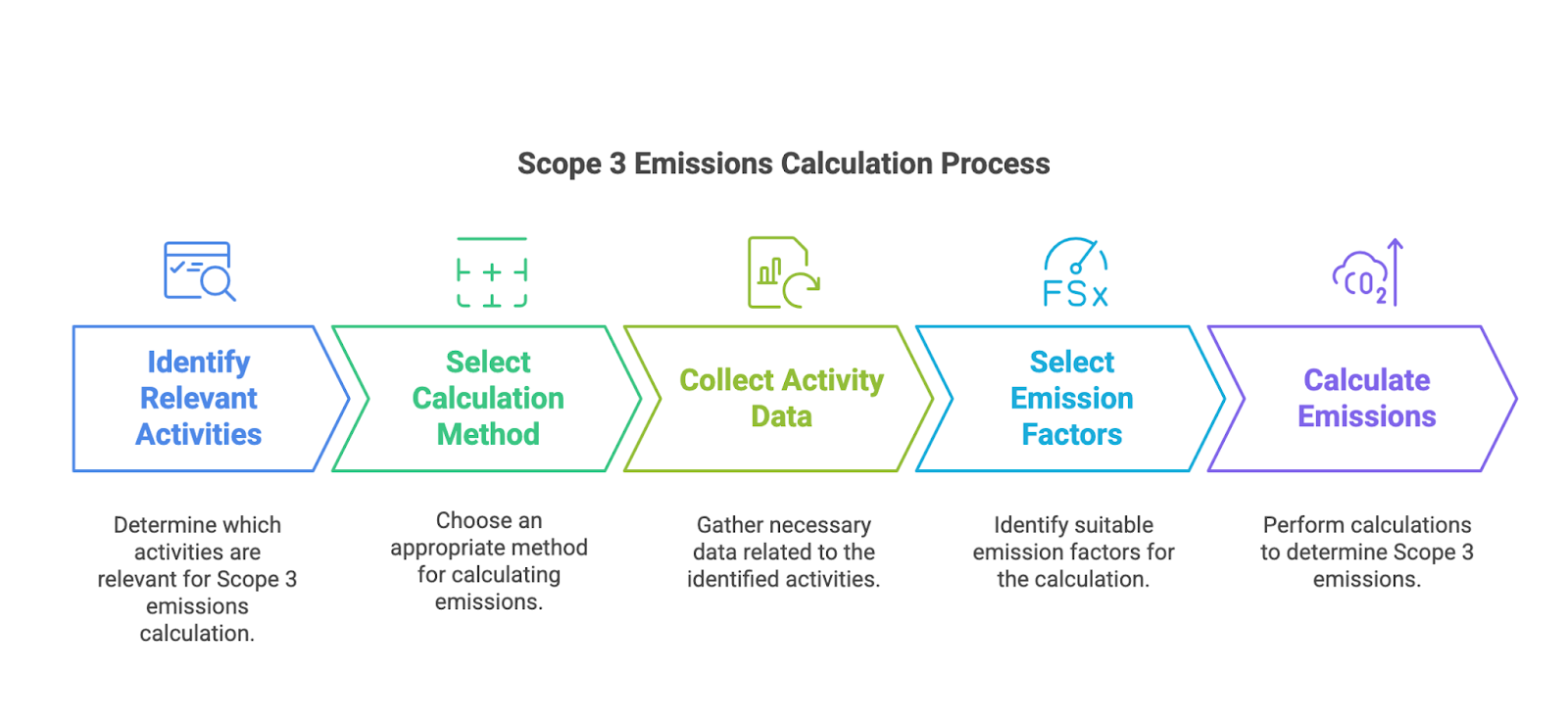

Calculation Requirements

For each Scope 3 category:

- Identify relevant activities

- Select calculation method:

- Supplier-specific method

- Average-data method

- Spend-based method

- Hybrid method

- Collect activity data

- Select emission factors

- Calculate emissions

Example: Calculating Category 1 Emissions

For purchased goods using spend-based method:

- Annual spend on steel: $1,000,000

- Emission factor: 3 kg CO₂e/$

- Calculation: $1,000,000 × 3 kg CO₂e/$ = 3,000,000 kg CO₂e

Implementation Guidance

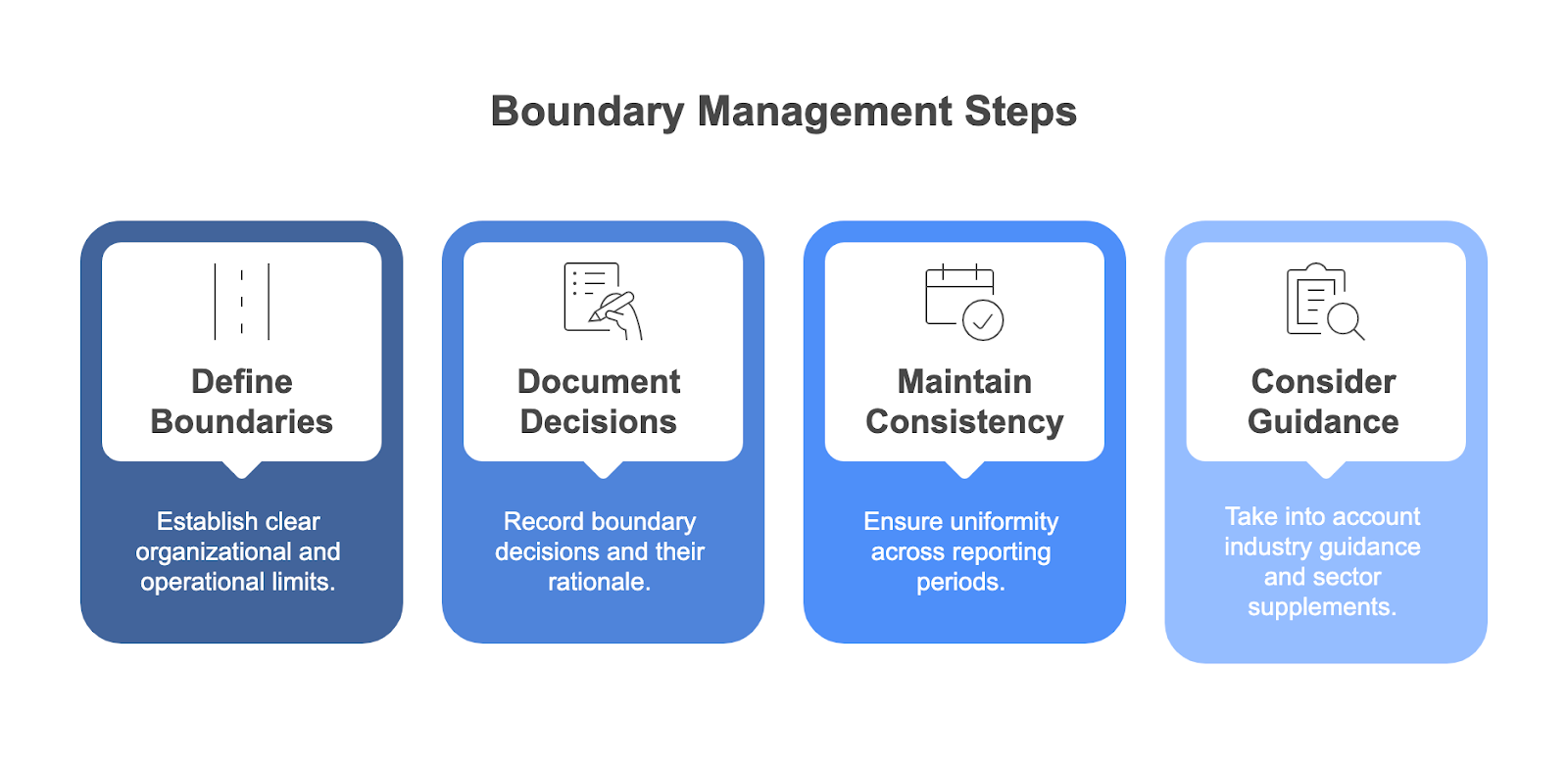

Setting Boundaries

- Define clear organizational and operational boundaries

- Document boundary decisions and rationale

- Maintain consistency across reporting periods

- Consider industry guidance and sector supplements

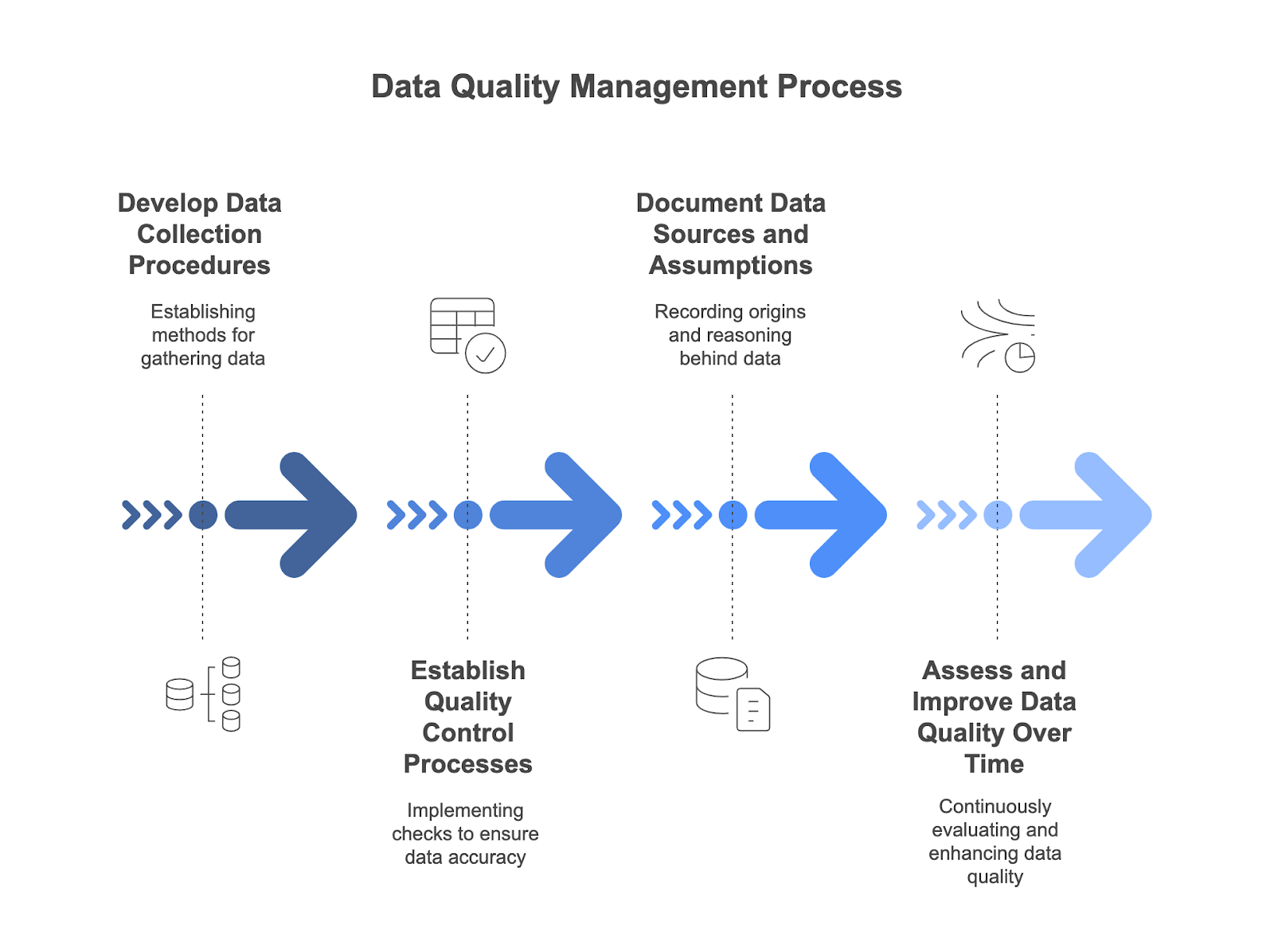

Data Collection and Quality

- Develop data collection procedures

- Establish quality control processes

- Document data sources and assumptions

- Assess and improve data quality over time

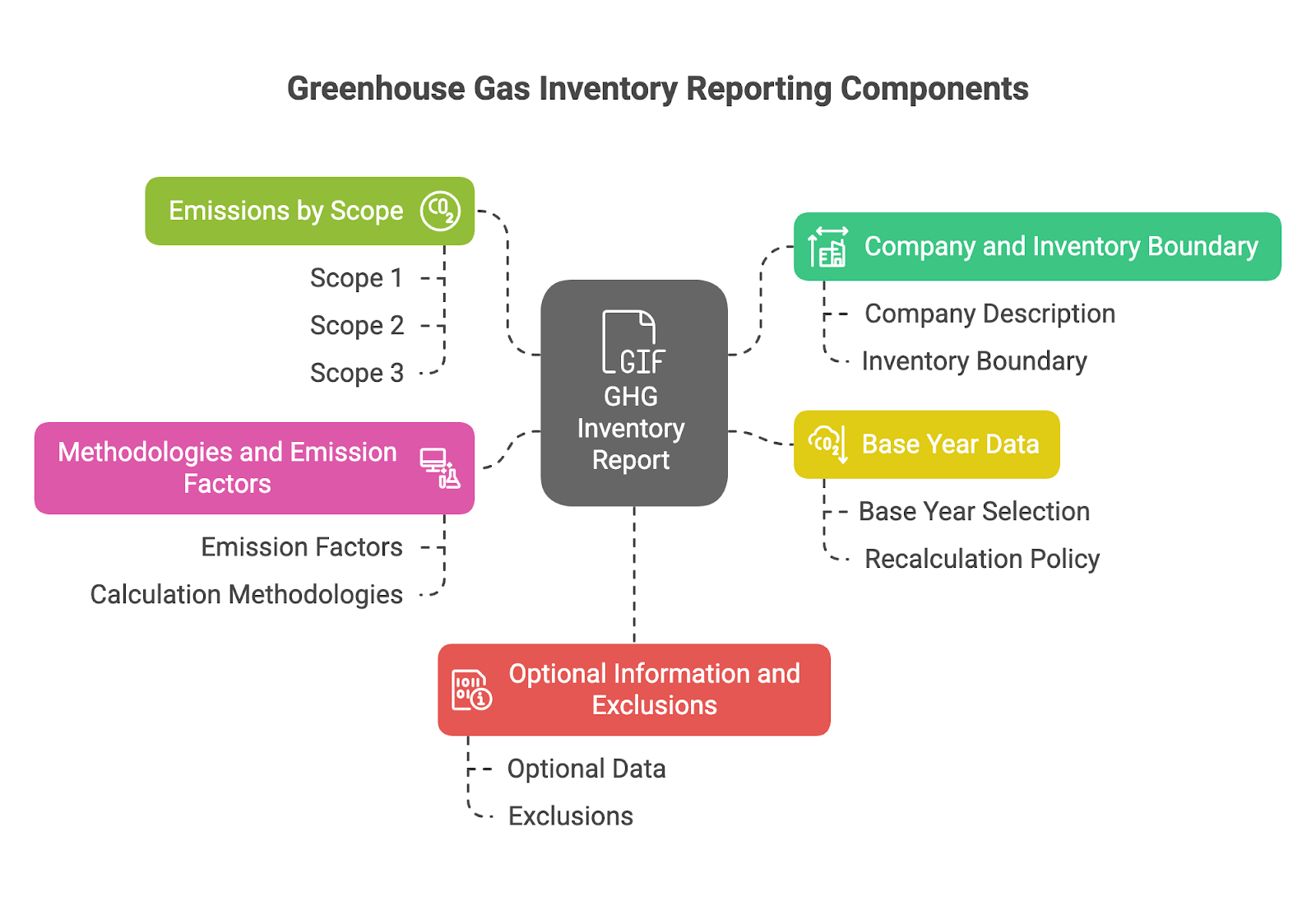

Reporting Requirements

- Description of the company and inventory boundary

- Information on emissions by scope

- Base year emissions data and recalculation policy

- Description of methodologies and emission factors

- Information on optional information and exclusions

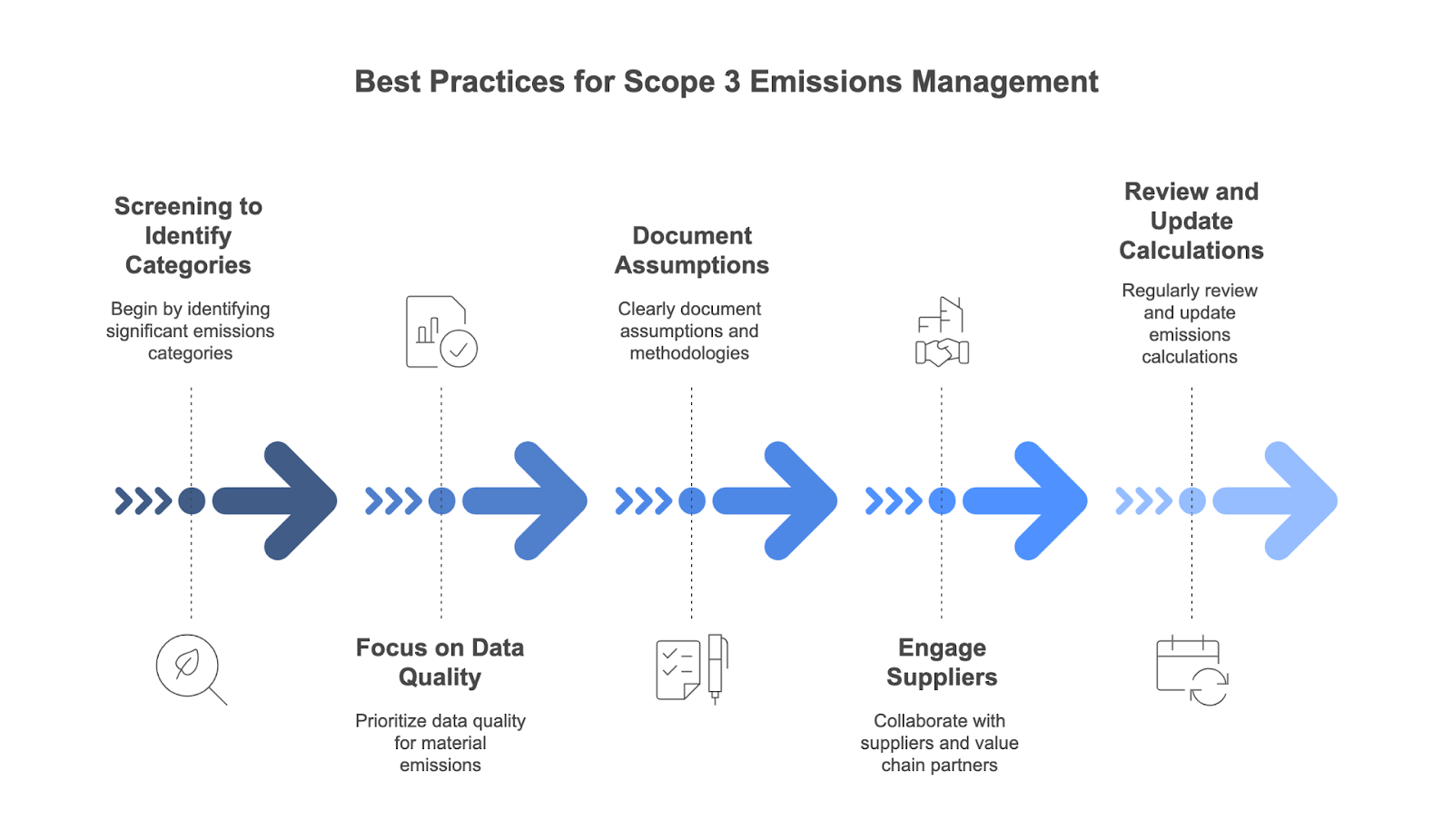

Best Practices:

- Start with screening to identify significant categories

- Focus on data quality for material emissions sources

- Document assumptions and methodologies clearly

- Engage suppliers and value chain partners

- Review and update calculations regularly